Guest article – The duty-free categories and concepts that will count as we approach 2030

In the fourth in a series about the future of European airport concessions compiled by Blueprint with data from ACI, we examine the categories and ideas that will rise above the rest as passengers look for a rebooted, re-energised duty-free offering. Click here for part one in the series, here for part two, and here for the third part.

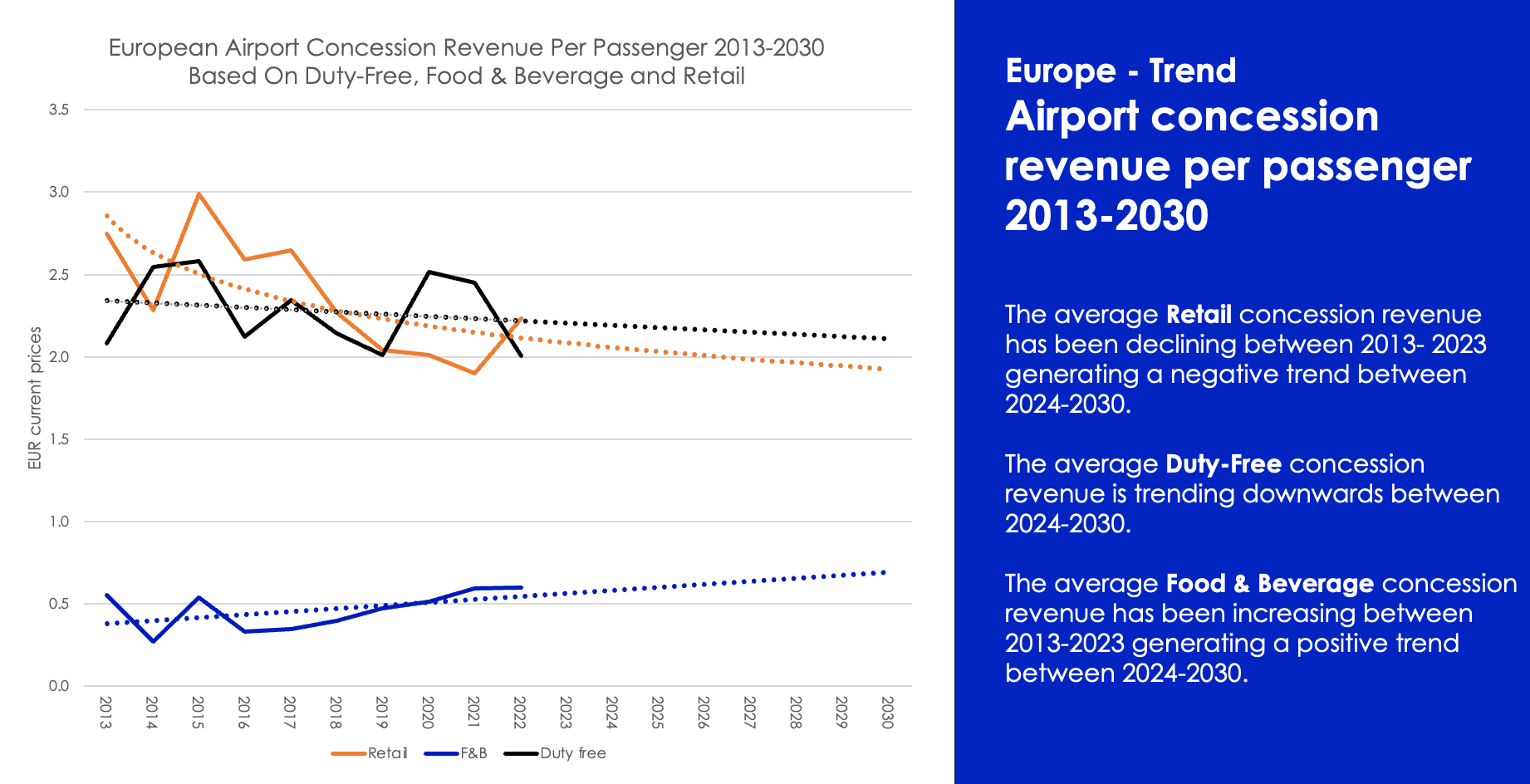

In a travel environment where passenger spend per head is falling, European airports must look more closely at their retail offers, in particular their pricing, product category mix and store layouts.

“It should send shivers down our spines, when airport duty-free concession per passenger continues to trend downwards,” comments Blueprint Partner Thomas Kaneko Henningsen. “Duty-free store concessions are a critical revenue channel for airports, but how to lift it needs some rethinking.”

This feature takes a closer look at what might be in store for price advantage, how the biggest product category – beauty – is trending, and new store layouts.

Why competing on pricing is no longer enough

Historically, airport duty-free stores’ value proposition has been based on offering travelling shoppers a price advantage – a legacy dating back to 1947 when the first duty-free store opened at Shannon Airport in Ireland. As airports evolved, duty-free stores became the very bedrock today’s travel retail is based on.

In the past decade, duty-free stores have been facing intense competition when it comes to maintaining price advantage and travel value positioning. Rival ecommerce platforms benefit from powerful price search engines and domestic markets often offer greater value for money and prioritise sell-through.

On top, the domestic market has succeeded at evolving factory outlet stores into highly sophisticated premium outlets where shoppers purchase quality brands at cheaper prices. Today’s domestic market shoppers are spoiled for choice when it comes to accessing great products at lower price points.

Adding to this equation is the fact that best-selling product categories within duty-free stores are facing other pressures. The speed and intensity at which US tariffs are arriving in the global market could not have been predicted just a few months ago. The comprehensive tariff announcement from the Trump administration on 2 April backtracked on the 200% tariff on alcohol from France and other European nations but has escalated global trade tensions.

In North America, Canada’s duty-free sector is already being hit hard with border stores facing sales declines of up to -80% as traffic between Canada and the USA stalls.

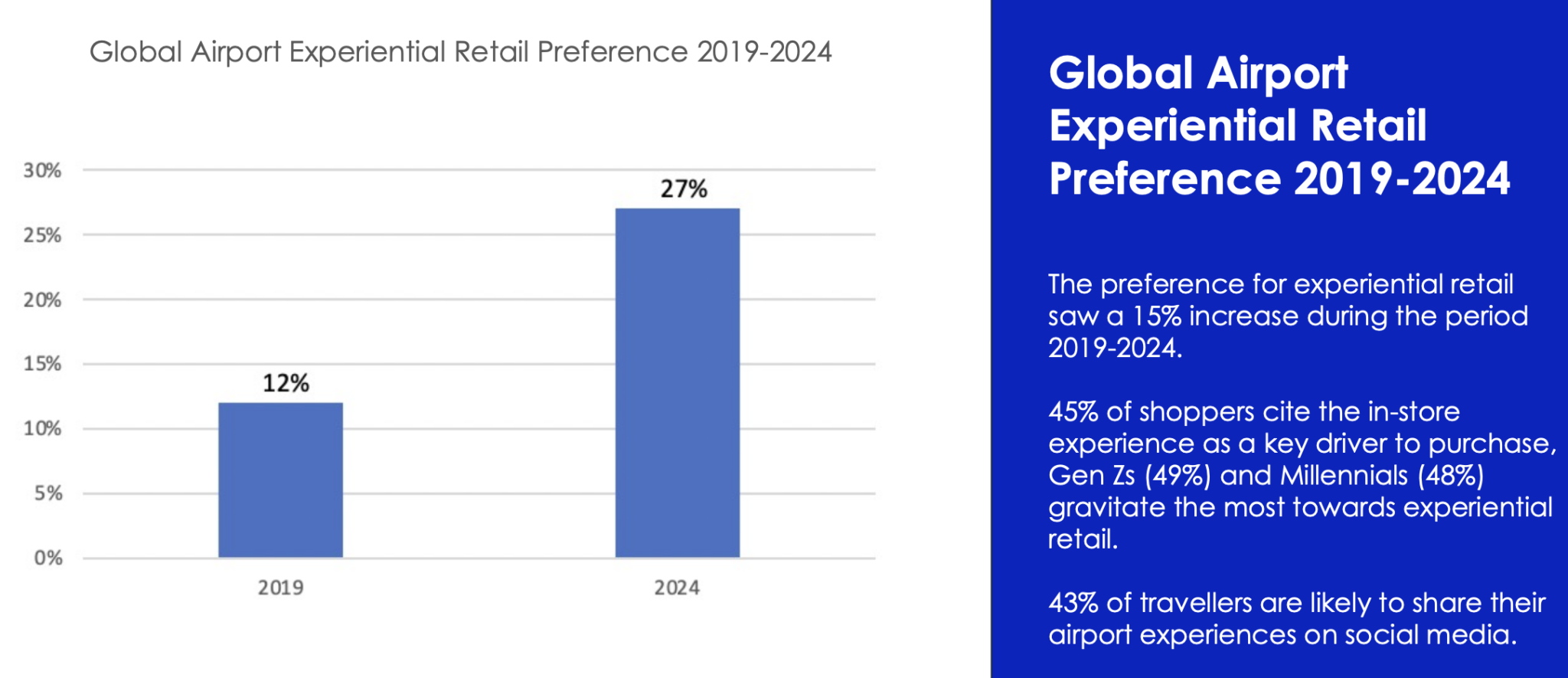

Whichever categories airport retailers focus on most towards 2030, they will all be underscored by the growing passenger expectation of more experiential retail. According to m1nd-set research, this preference has jumped from 12% in 2019 to 27% last year – more than double, and experiences are now considered more important than pricing advantage. During the same period the importance of price advantage dropped from 30% to 13% among travelling shoppers.

Is beauty still a safe bet?

“The beauty category combined with price advantage will continue to play an important role within duty-free stores, the reason being that impulse purchasing in airports remains high,” said Kaneko Henningsen. “Parallel to this, we will see experiential shopping stepping up and becoming an industry standard on a global scale. It is that long-lasting feeling of personal, immersive and emotional shopping experiences that will drive spend and revenue in duty free.”

Beauty is travel retail’s biggest category, and in the global domestic consumer market it is expected to be a growth leader. According to McKinsey, perfumes and fragrances hit US$446 billion in 2023 and will have a CAGR of +6% to 2028, though some regions such as the Middle East & Africa are projected to reach +10%.

While skincare takes the biggest share of sales, and will continue to do so in 2028, the current smallest sub-sector of fragrances will grow at +7% CAGR, outpacing the rest. Travel retail stakeholders will know that fragrances have been a powerful sales driver in recent years. McKinsey says the sub-sector posted the highest growth (+14%) in 2023. This is going to moderate in the coming years, but fragrances will still lead beauty’s growth.

Much of the beauty market’s forecasted growth will be propelled by younger generations embracing beauty products at an increasingly younger age. According to Forbes and Grand View Research, the global children personal care market is projected to hit CAGR of +6.2% between 2022 and 2030. In 2021, this market sector was valued at US$7.5 billion driven by high disposable incomes, heightened focus on personal grooming and the influence of social media platforms.

Within the beauty category, travel retail and speciality retail channels are forecasted to hit CAGR of +9% and +8%, respectively, between 2023 and 2030. Ecommerce is projected to lead with +12% CAGR, underlining how shoppers continue to lean on availability, accessibility, convenience and above all price transparency.

Other categories set for high CAGRs in the domestic market include eyewear, projected to grow at +8.4% annually (Allied Analytics LLP). Sunglasses, and eyewear in general, are in vogue thanks to so many celebrities on social media donning shades, often to avoid the spotlight, but giving brands great publicity in the process.